Inseego’s Huge Turnkey Enterprise Network Business Opportunity (NASDAQ:INSG)

imaginima/iStock via Getty Images")

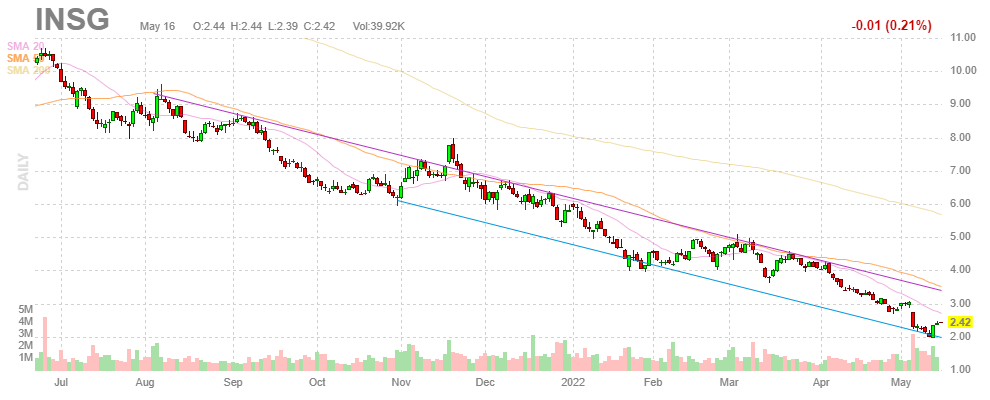

Inseego Corp. (NASDAQ:INSG) has had a very rough time after the height of the 4G/work-from-home rally that took the shares to $20 early last year.

FinViz

But even then the seeds of an even bigger wave were visible:

- 5G;

- Enterprise market;

- SaaS platform.

All three of these were growing fast already (although from a small basis), and all three were supposed to bring higher gross margins. The bad news is that this has happened slower than we expected, and in the meantime, the finances are really ugly.

But on the positive side, the next wave is gathering momentum. 5G sales are up significantly, boosting gross margins, and enterprise sales are starting to take off often with the SaaS platform attached.

Enterprise 5G Edge Cloud

The enterprise market was always very attractive because it’s 3x the size of the carrier market and margins are usually higher here. Inseego partners with carriers, most notably T-Mobile (TMUS), for enterprise sales.

But the company is going much further. It proposes a turnkey WAN solution that is easy to implement and enables enterprises full control from a single pane of glass. Here is the state of the usual enterprise WAN (Q1CC):

Current enterprise WAN architectures are complex, highly fragmented, expensive to maintain, and dependent on costly on-premise appliances and brittle third-party integrations. They’re also saddled with multiple management consoles and multiple policies. This large attack surface area makes them rather vulnerable to cyberattacks. Inseego clients on transforming the enterprise WAN market by offering the full stack of networking capabilities as a 5G cloud app.

5G is fast enough and much more flexible so it can provide enterprise networks on the cheap and the extent to home working. The architecture consists of three parts:

- Inseego’s FWA (fixed wireless access) products and mobile hotspots;

- Inseegos’s SaaS platform enables enterprises to move their corporate LAN into the Inseego 5G Cloud;

- Ctrack’s asset tracking solutions.

The SaaS suite is undergoing significant improvements, but will afford enterprises:

The software is the key technology that is powering our 5G Edge cloud where we are bringing all these pieces of our solutions together. This critical layer of software is key to allowing enterprises to move the corporate LAN into the Inseego 5G Cloud. Then, introduce this to the market in the near future, our enterprise customers will be able to innovate at the edge and empower a more secure distributed workforce or branch locations or a 5G network fabric for the first time.

They already have clients implementing this, further illustrating the advantages of their architecture (Q1CC):

One example is an enterprise customer with over 27,000 employees. They were looking for a reliable 5G work from home solution to offer their remote employees to ensure a secure and consistent user experience no matter where they were located. To ensure security and consistency, the customer is now using our cloud management solution so that their IT team can have visibility into the entire deployment, enabling them to manage, configure, and monitor the connections all from a single pane of glass.

The surprising third element is that they are integrating their asset tracking business Ctrack as the third pillar of their 5G Cloud App, after making significant enhancements and integrating it into their 5G Cloud.

Ctrack was a separate business (called Enterprise SaaS) serving thousands of SMEs and is mostly used for tracking vehicle fleets (and equipment at some airports), but the potential here is much larger especially when integrated with the basic enterprise network. The potential for synergies are large here (Q1CC):

We see a huge opportunity to utilize this technology to digitize many facets of enterprise operations in verticals such as transportation, construction, logistics, supply chain, energy, utilities, services, local governments, and more.

One might also point out that Ctrack is a much higher-margin business. Apart from some hardware (trackers), it is SaaS-based, fetching gross margins almost twice the company’s 27.3% average at 53.3%

In short, the company will offer flexible 5G-based enterprise networks that are easy to manage, configure, and monitor, all from a single pane of glass. In addition, the company offers an integrated asset tracking solution that can capture the location and performance of the company’s assets.

And they have many partners in carriers, apart from selling mobile hotspots and access points to the carriers. These partner with Inseego to get enterprises onto 5G, where they can win business from cable and other network solutions.

5G is also the technology par excellence to close some of the digital divide, and Inseego is involved in this with a deal with US Cellular and a deal with one of the top public libraries in the U.S. with over 90 branches.

Short-term headwinds

It’s not all going to be plain sailing, as there are a number of bottlenecks:

- Supply chain issues (the cost and availability of freight and prices of components);

- China lockdown;

- Carrier enterpr

ise dataplans.

The supply chain headwind did prevent the 200bp gross margin expansion (to 27.3%) from being even bigger, and the Chinese lockdowns are producing further problems (Q1CC):

we remain wary that ongoing supply chain challenges associated with COVID-related lock downs in China could impact our new product launches later in 2022.

Management sees an ease fairly soon. Any delays will be measured in months, not quarters or years. The carrier enterprise data plans are now coming online as well. So, this can produce some delays, but no fundamental change in the company outlook (Q1CC):

And we’re really ready-to-go like we’ve got the portfolio; we’ve got the products. And we’re super excited about all the pipeline of opportunities we are working through with lots of hundreds of enterprises right now. So to me, this is more of a delay and if I were to talk about how you model it that I would just say you model it as a delay versus the demand leaving us or so anything like that.

The company is also able to offset some of the cost increases into pricing by increasing some prices (depending on the market).

Finances

The finances, of course, still make for grim reading:

- GAAP loss of $25.2M;

- Non-GAAP net loss of $12.1M;

- Adjusted EBITDA loss of $3.3M;

- Cash and equivalents $45.2M, down from $49.8M at the end of Q4/21;

- Debt (2025 notes) $157.6M;

- The company paid $2.9M in interest cost and $661K on dividends on Series E preferred shares.

On the other hand, there is progress as well:

- Revenue +23% (pro forma, ex sale of Ctrack South Africa, sold in Q3/21) to $61.38M;

- 5G revenue was 142% y/y and comprised 44% of total revenue (was 38% in Q4);

- 5G + SaaS was revenue rose 68% and now comprises 67% of revenue (up from 58% in Q4/21);

- The company launched a 5G solution with TELUS Canada;

- The company received orders from US Celluar FWA deployment in 10 cities with dozens more cities planned for the rest of the year;

- The company received repeat orders from several international customers;

- The company closed a deal with one of the top public libraries in the U.S. with over 90 branches;

- The company won a new carrier customer in the Nordic countries, with shipments already starting.

So, Q1 was almost on track for that 25% FY22 growth. The parts that matter are growing very fast, and we’re not seeing that coming to a halt anytime soon as (Q1CC):

Speaking of FWA, we are encouraged by the continued growth in our pipeline but more importantly, we are seeing several customers move to deploy our products broadly across their organizations. These engagements follow a typical pattern where an enterprise will buy three to five plus devices to test. Thereafter they order 30 to 50 devices for small scale deployment before rolling out company wide, which in many cases required 1000s of Inseego devices. These customers are also leveraging our cloud-based software to manage and secure the devices across their distributed workforce or branch locations.

There are uncertainties, but these are delays at best, with no cancellations of orders. On the Q2CC, management will give an update on whether the 25% revenue growth for FY22 and being free cash-flow positive by year-end are still in the cards. Investors are not taking any chances, needless to say.

It will also provide more details on revamping Ctrack and integrating it into their 5G Edge Cloud, which we think is a terrific idea, as we don’t know of any company that provides enterprise 5G LAN solutions with integrated asset tracking to boot.

Cash

The most worrying part of the company is their debt and the continued losses. They managed to keep cash outflow relatively limited in Q1 by some favorable working capital changes, but how long they can continue with the losses remains very much to be seen.

They are saved in a way by a ridiculously high stock-based compensation at $11.2M in Q1, which amounts to 18% of revenue. While this is a non-cash item, of course, so it greatly helps limit the cash bleed, it’s not something to rejoice for shareholders.

Cash should be plenty for the original FY22 guidance (revenue growth of +25% and being free cash flow positive by the end of the year), but the possible delays in achieving this could very well make this more problematic.

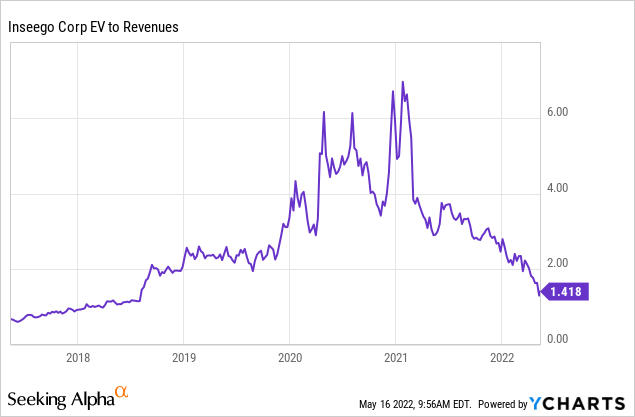

Valuation

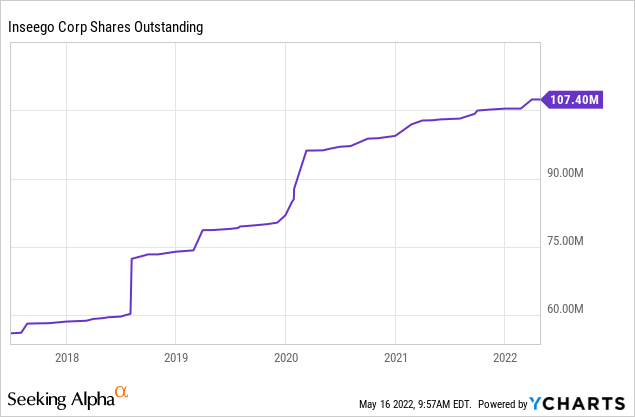

And the company had to resort to issuing shares:

On April 27, 2022, there were 107.4M shares outstanding, 4.9M stock options, and 2.5M warrants (although the latter have an exercise price of $7 and expire by the end of June so they’re not going to count). There are also 14.3M notes but these count under debt ($157.6M).

That is, the company has a market cap of $250M and an EV of some $370M, so the shares are selling at 2x EV/S. That’s still not cheap, but keep in mind that the relevant parts of the company are growing at 60%+

Conclusion

There are quite a few things to like:

- The company is rapidly growing its 5G, enterprise, and SaaS business and all three are producing higher gross margins;

- The 5G and enterprise markets are still in the very early innings;

- The company is offering an attractive one-stop-shop for 5G enterprise networks and folding its asset tracking business into its enterprise network solution;

- The company is still gaining traction in the carrier market and many carriers partner with them for the enterprise market.

But then there are the negatives:

- Large net loss;

- Stagnant 4G market;

- Cash bleed;

- Large debt;

- Large share-based compensation.

We think the positives will ultimately prevail, as these are long-term trends, and there is evidence of the company’s rapid growth in 5G, winning carriers and enterprise customers, along with gross margin improvement.

That win looked to be Q4, when the cash bleed was supposed to come to an end. However, the China lockdowns could very

well have pushed that back one or two quarters, something that remains to be seen.

The risk is, of course, that the company will need additional financing. Funnily enough, the cash bleed is greatly reduced by the high stock-based compensation, which in a way serves as a sort of saving grace.

We are confident the $45M of cash is enough to last them until the end of the year, but if there are further delays, this could get more problematic.

In any case, we think that next year we could have a whole different company in front of us, given the opportunities they have in the enterprise market and the clever way they’re positioning themselves, which is already starting to pay off.